Disaster Startups and the Advice I Give Most Often

By: Jeff Schlegelmilch

I am often approached by entrepreneurs looking for advice on their idea or product that they are developing. Usually this involves a piece of technology that has strong potential, at least from a logical point of view, in disaster resilience. Before going into the advice I give, I wanted to gut check my anecdotal experience to see what some of the broader trends are, so I did a quick and dirty analysis. By no means is it exhaustive or even a scientifically rigorous. But it provides some interesting insights and possible explanations for the trends in this landscape. The scope of this analysis was for the decade 2014 - 2024. This cutoff is intentional to avoid reporting latency that could impact the availability of data for late 2025, and 2026 to date. As a result, near(ish)-term impacts to this landscape are likely not reflected in the analysis below.

The Startup Landscape

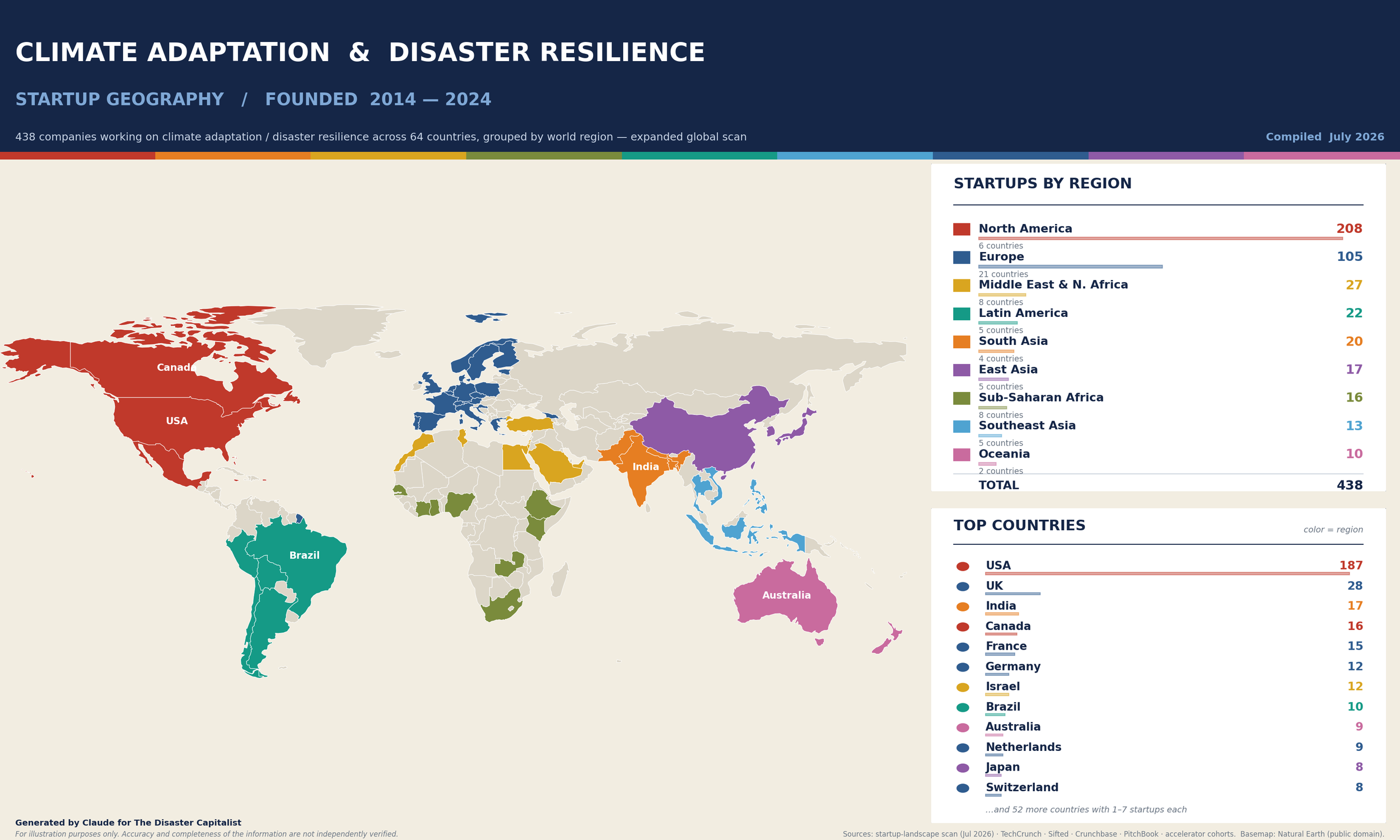

In Figure 1, we see the majority of startups being founded between 2014 and 2024 are in the United States. Although this may be an artefact of the sources used, and the registration requirements and search-ability of startups; data availability from different countries is also certainly a limitation. This also does not capture emerging non-profits, or other good ideas emerging in different ways. However, this does not seem overly surprising, although this could change with ongoing efforts to attract tech startups and other entrepreneurs in other parts of the world. This analysis spans 438 companies across 64 countries, grouped by world region, and the basic picture holds: North America still accounts for the largest share (208 companies), followed by Europe (105), with the United States alone home to 187 — well ahead of the United Kingdom and India, the next-largest single countries in terms of startups.

Figure 1 — Climate Adaptation / Disaster Resilience Startups by Region and Country (438 companies across 64 countries, founded 2014–2024)

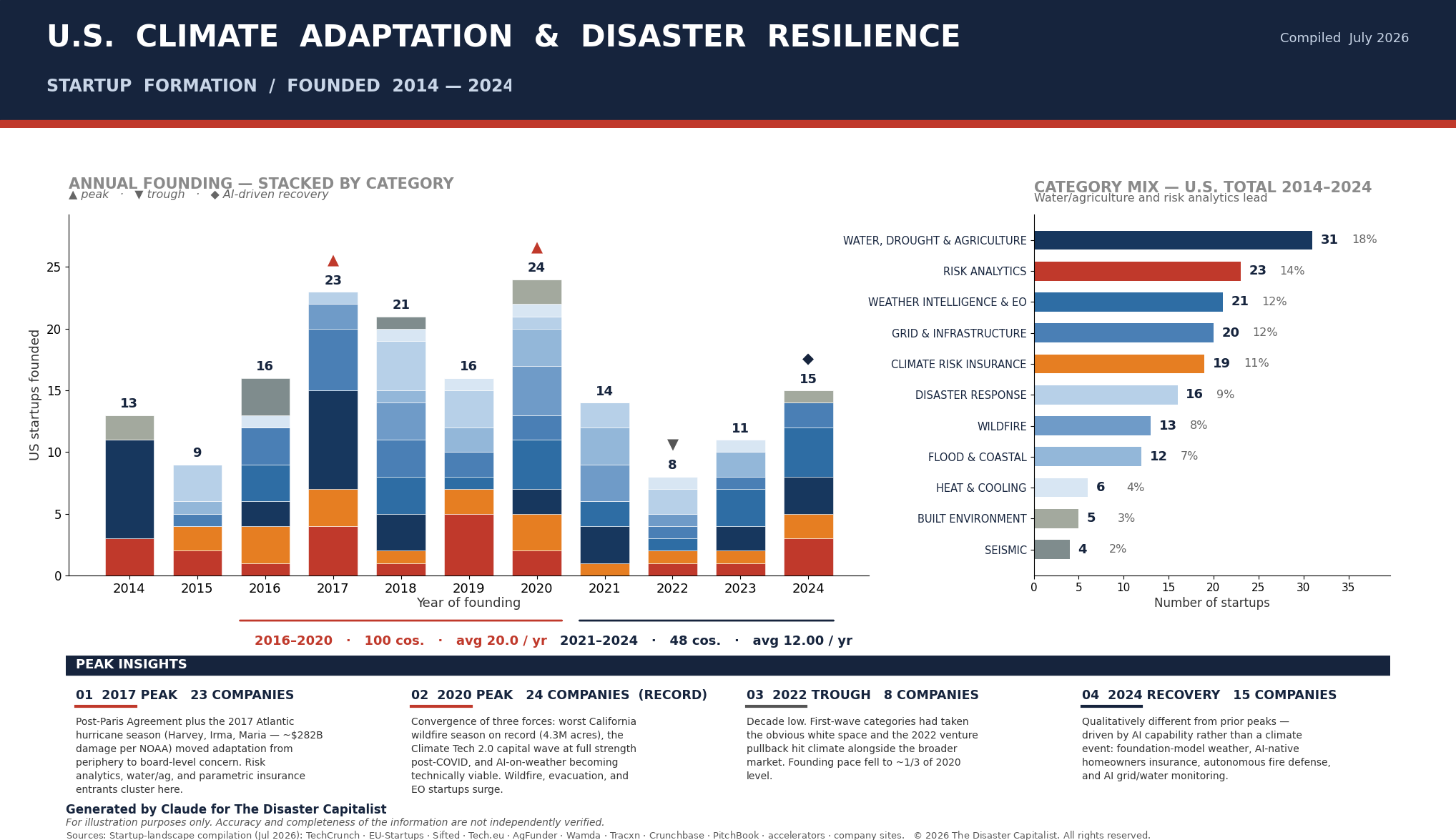

In Figure 2, we find that the largest driver is solutions related to water, drought, and agriculture, which lead both the global mix (105 companies, ~25%) and the U.S. mix (31 companies, ~18%). Risk analytics — products looking at threats to property, infrastructure, and/or investments — is a close second (~16% globally, ~14% in the U.S.), followed by weather intelligence and Earth observation.

Even more interesting is that the pattern in the United States seems driven by a mix of events and policy. The Paris Agreement coincided with some particularly harsh hurricane seasons which brought a lot of these issues and needs front of mind. I suspect it was more the impacts of the disasters rather than the Paris agreement that drove this, but political priorities post Paris should not be ruled out. We see a bit of a lull after the 2020, with a broader venture capital pullback, among other potential factors. But then the AI boom seems to have translated into a surge in startups in 2024.

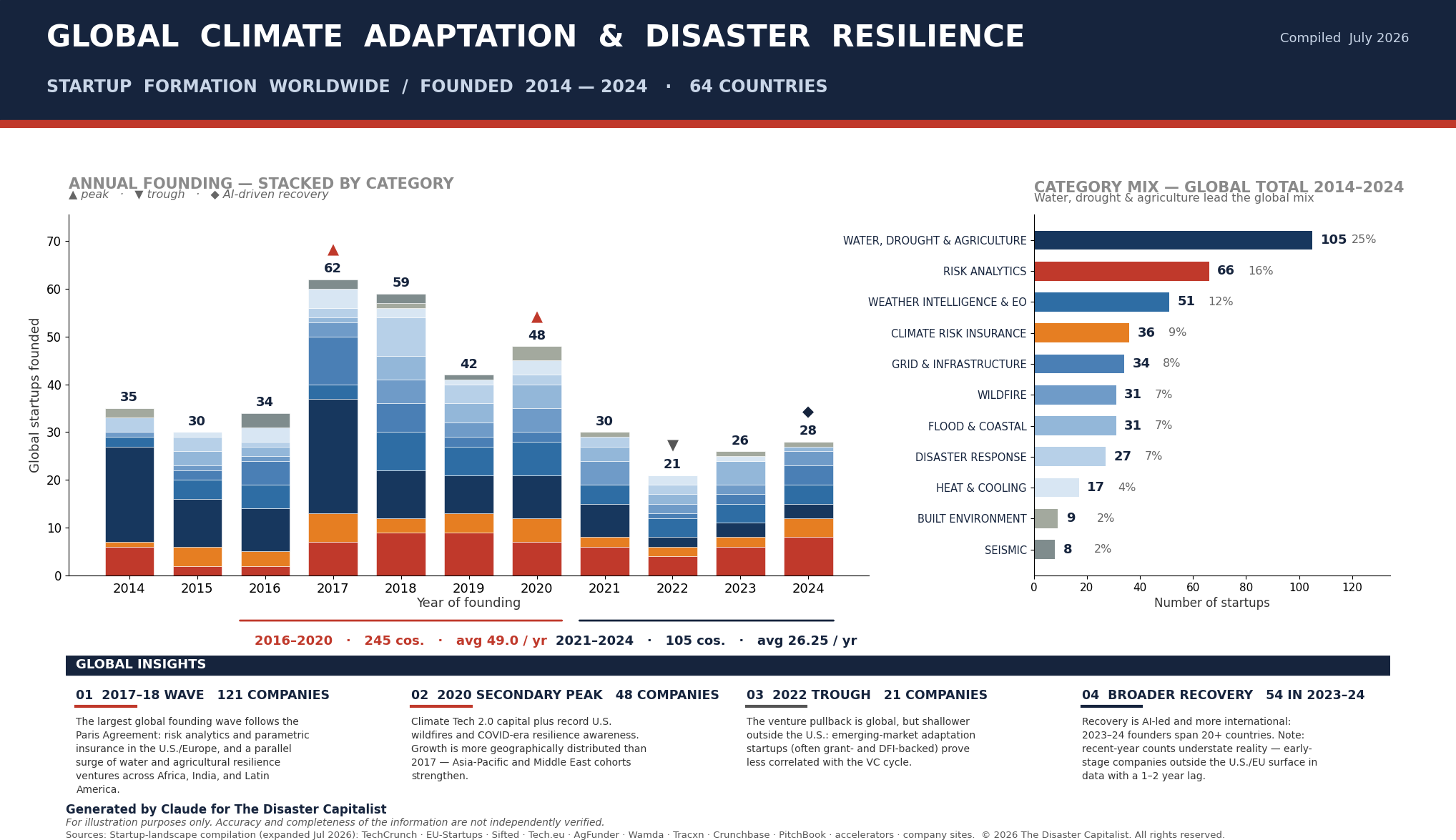

Figure 3 widens the lens to the full global dataset, and the same rhythm holds beyond the United States: worldwide founding peaks in 2017 (62 companies) and again in 2020 (48), falls to a decade low in 2022 (21), and then recovers across 2023–2024 (54 companies) in a wave that is both likely more AI-driven and more geographically distributed, with recent-year cohorts spanning more than twenty countries.

Figure 2 — Climate Adaptation / Disaster Resilience Startups in the US by Year and Type (170 companies, founded 2014–2024)

Figure 3 — Global Climate Adaptation / Disaster Resilience Startup Formation by Year and Category (438 companies across 64 countries, founded 2014–2024)

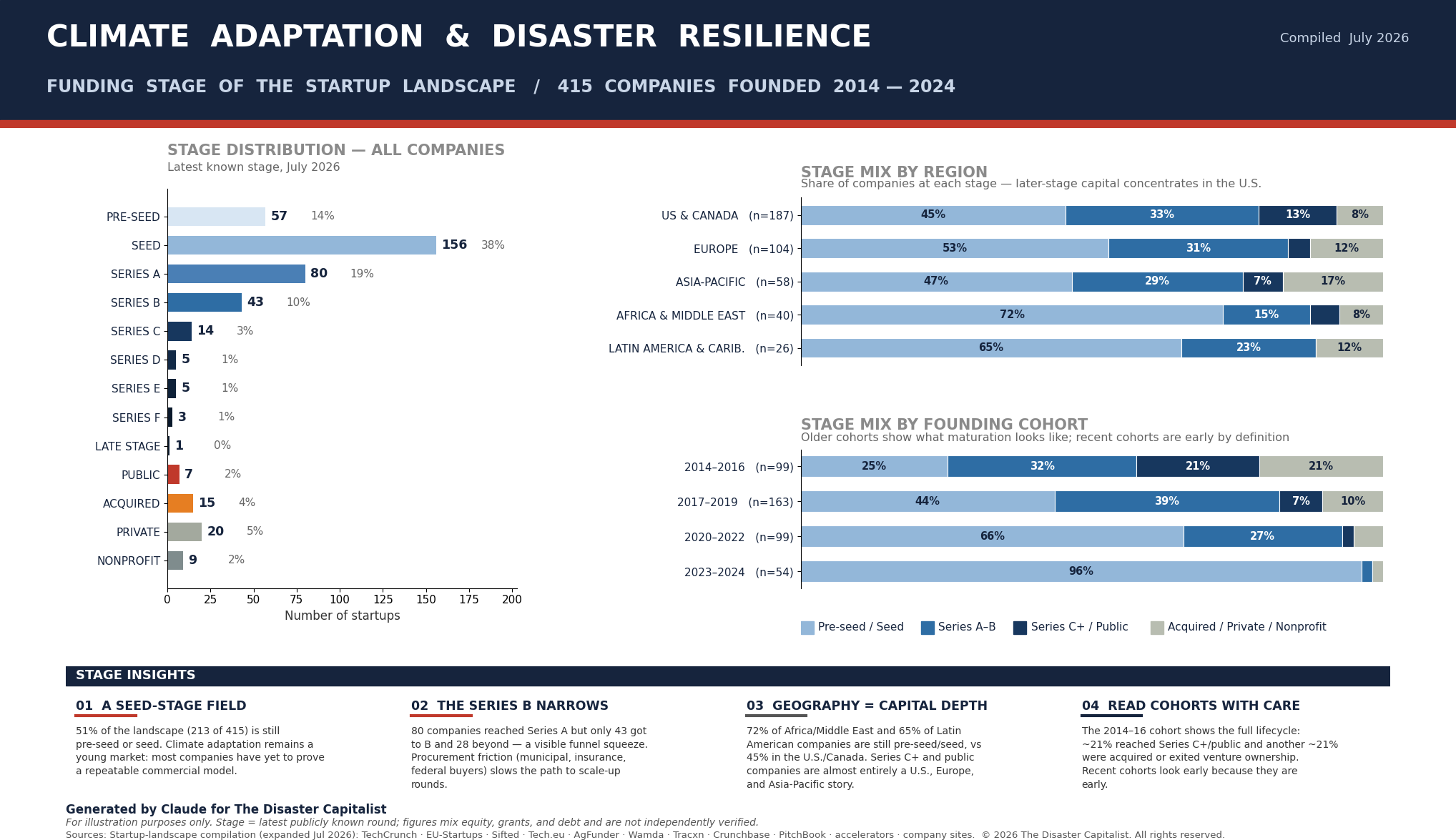

Figure 4 rounds out the picture by looking at how mature the field is: of the 415 companies with a known funding stage, roughly half (51%) are still at pre-seed or seed, and while 80 have reached Series A, only 43 make it to Series B. That funnel matters for the advice that follows — this is still an early-stage market where getting to scale depends less on a clever idea than on clearing the procurement and revenue hurdles that thin the herd between the seed and growth stages.

Figure 4 — Funding Stage of the Climate Adaptation / Disaster Resilience Startup Landscape (415 companies founded 2014–2024)

Anecdotally speaking, the startup scene seems to be continuing to grow in the years since 2024 despite it not being included (yet) in the charts here. This analysis stops at 2024 in part due to latency in data and retrievability of startups from public sources over the past year. Additionally, the full impacts of shifts in climate and disaster policy in the United States and elsewhere are still rippling through the landscape. How this may shift responsibility from primarily government functions to sub-national and private sectors is still playing out. This may foster more innovation by necessitating tools, like AI, to do more with less. But it may also impede investment by decentralizing upstream purchasing and spending priorities. The full impact remains to be seen, but as always, the market will continue to adapt.

The Most Common Advice I Give

Good ideas from a founder does not necessarily translate into market viability. The nuances of human behavior and organizational procurement practices can make this a challenging landscape where good ideas in the lab can’t get off the ground in the open. When approached by startups, or those considering developing a startup, the most common advice I give is often a variation of the following:

Need does not equate to sales

Many startup ideas are great solutions to disaster challenges, in theory. But in practice an organization needs to see it is a good idea in a sea of competing priorities and insufficient budgets. And more likely you need to do this across multiple organizations. Getting someone to invest in purchasing something and then implementing something for a disaster situation is a hard thing to sell. Organizations need to invest in the product, as well as the internal change management process. It means implementing it into trainings, policies, and drills and exercises to build competency. These are all significant expenses in addition to the cost of the product itself. Unless it helps them meet a current requirement, or there is temporary money they can use that will go away, this is often a very steep hill to climb.

Successful examples I have seen have been available at a scalable price point to lower the initial risk and allow for piloting among early adopters to help foster internal champions, or they have responded to a new mandate or spending priority (e.g. grants to upgrade communications systems). Successful tools also tend to have non-disaster uses to help drive efficiency and productivity, with added features to help coordinate in a disaster situation. This creates a much more tangible and less risky endeavor for the prospective customer. But funding sources and procurement policies also matter, which brings me to the next point….

The market may not be the market you think it is

Many people come to me and say they want to “sell to FEMA”. This makes sense on the surface, right? Selling to the federal agencies is big business, with its own ecosystem of contract vehicles and a suite of software and consulting services designed to facilitate awareness and access to agency funding. FEMA is responsible for the disbursement of billions of dollars in disaster funds, and coordinates even more funding flowing in from across agencies. They buy a lot of stuff, for sure. But a lot of that money goes to States to reimburse them for costs under various programs. So in these cases, FEMA does not buy the stuff, States do. In that one preceding sentence, I just took a 1 customer strategy and increased it to 50+ (including territories and some tribal nations). Furthermore, some states delegate some effort to local and county officials, along with major urban areas that often have their own purchasing processes.

Maybe you want to be the primary company, or maybe you want to be a vendor for one of the big companies already established and already on the right procurement vehicles. It could be that your novel product may be the better deal on its own, but it is wrapped up in a package of services that a larger company can provide as an all-in-one package with one vendor to manage, rather than an à la carte of other companies. Look at the market in terms of who is buying, and with whose money. Also make sure and look at who else is selling, and how. You may be better off as a stand-alone company, or you may be a strong asset to a big player looking to differentiate themselves from others on the really large bids that you can’t compete on.

Subject matter expertise does not always translate into expertise in business, and vice versa

I have a colleague who runs a very successful technology-based non-profit. All of the finance bros always try to say how much money can be made if he took it public. But the main product is most attractive in resource poor settings. Settings where there is no market, but tremendous need. It appears to be very popular, but the purchasing power of the “customer” is virtually nothing. As a non-profit, however, the company gets a lot of money from corporate social responsibility funding, especially from industries related to the technology employed. Knowing how to create business value does not always translate into understanding how things work in the field. On the other hand, I have seen too many experts talk about a need to be filled in their agency, only to leave and create a non-viable product, or who are left wandering after unable to meet the demands of the firm that scooped them up when they left public service. It is one thing to know the needs in the field, but another to know how to create value for your investors.

The moral of the story is that you need both kinds of experts. Those in the business of building companies, and those in the field of climate adaptation / disaster resilience. Solutions come from those closest to the problem, and capital comes from a value proposition that limits investor risk, and enhances shareholder value.

The world of startups will continue to evolve as this field does. As climate impacts grow more frequent and costly, and as AI continues to reshape what’s possible, the pipeline of innovation entering this space will only increase. New investments — from government adaptation funds to private capital drawn in by growing infrastructure and insurance risks — will create opportunities alongside new layers of complexity to navigate. What remains constant is the need for solutions grounded not just in technical ingenuity, but in the real-world dynamics of how organizations prepare, procure, and ultimately respond. The startups that master that combination will matter not just as businesses, but as critical contributors to how communities survive and adapt in an increasingly uncertain world.